The post Money, money, money. Must be funny. In a rich man’s world… appeared first on .

]]>There seems to be a weird relationship the majority of us have around money. So often we lose our power when the subject comes up. We find it a difficult to discuss, let alone ask for money for the services we offer. We whisper our fees and terms, start to sweat, or even discount the fee right on the spot. Many of us simply avoid the topic of money all together, and divert the conversation to something completely different. But of course none of this serves us at all. Money, or abundance, is such a central part of our life and actually helps life flow. We need to learn basic skills for these discussions and to love and embrace the topic rather than fear it.

When you run your own business, being able to talk about money, without fear, is a critical part of the daily conversations – and it needs to be. After all it creates the survival of your business, helps pay the bills and ideally, is what allows you to make a profit and live the life you dream. Understanding human behaviour toward money (including your own) can help you understand how customers behave around money too.

Did you know that you (and all humans) fear loss more than you value gain? You do this at a ratio of 2:1. This means that you prefer to stay in a situation that you are in, even if it isn’t good for you. What is the implication of this in business? It means even if you know a product or service is good for you, your default position is the status quo. This default position remains the same until you emotionally engage with the product or service and this tips you over to disrupt your status quo. Your customers are exactly the same. Customers will fear losing not only the position they are in, they will also fear losing the money they are about to part with for your product or service. Even when you know something is good for your customer this fear of loss is one of the reasons they simply cannot make the decision to purchase it and walk away.

You physically feel pain when you pay. Seriously! The insula (or insular cortex) in the brain fires when you are about to part with cash. This is one area of the brain associated with anxiety and pain. No wonder it hurts to pay. You literally have the pain of paying.

Have you ever seen Apple discount their products? No. Never. Why? They know that discounts permanently damage the perceived value of the brand. So when you’re thinking about having a discount to bring in some short-term revenue, be aware that the relative value now associated with your brand is reduced forever.

There are many factors involved in the interaction and association we have with money. Understanding some of these not only helps put customer decision-making and judgement in perspective. You can learn to use some of these aspects to the financial advantage of your business.

Instead of fearing money it is time to embrace it. Make money your friend. Love the numbers and start to see and feel a shift in your relationship and power with money.

Sonia Friedrich is a Mentor and Strategic Consultant to Multimillionaires and Business Owners. She’s launched a new DVD that you can download or stream or purchase as a hardcopy – How to Set Fees and Terms – for Consultants and Service Providers. If you would like to find out more visit www.soniafriedrich.com.

The post Money, money, money. Must be funny. In a rich man’s world… appeared first on .

]]>The post The importance of your credit score appeared first on .

]]>

You might think the ability to pay back debt would the most important criterion for borrowing money, but it’s not the only one, writes Campbell Korff.

A young couple came into the branch in Ballina the other day looking for a loan to finance their first home. After getting a little background on their income and savings, it was clear that their dream of buying a home was attainable financially.

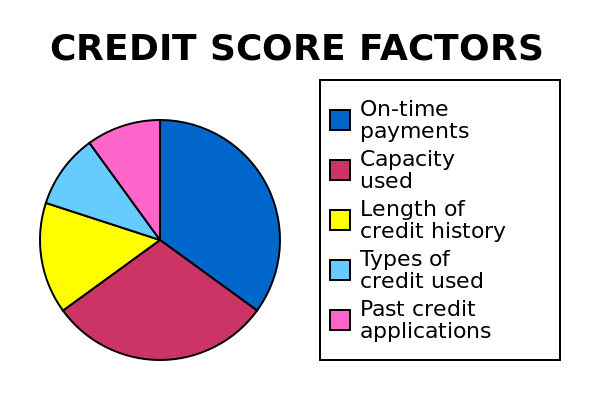

However, ability to repay debt is not the only criteria used by most lenders. Lenders are also concerned to establish that a borrower has the willingness to repay as well. This sounds trite, but what they mean is that the borrower has demonstrated that they are sufficiently diligent and reliable to comply with credit terms over time. These days, this question is often answered by a statistical record known as a credit score.

Unfortunately for the couple in question, despite a clear record as far as defaults are concerned, they failed to reach the benchmark set by the many lenders who credit score. This is because their current bank had regularly offered them increased limits on their credit card as their financial situation improved. Ironically, this proved their undoing, because with each increase the bank lodged a “credit enquiry” on their credit record, negatively impacting their score.

While we were able to place them with a lender who doesn’t credit score, this narrowed significantly the number of lenders available to them and increased their borrowing costs.

A credit score tracks your application for and repayment of debt. Obvious debt includes a mortgage, car finance and credit card, but phone companies and other utilities also run credit accounts.

“Their banks had offered them increased

limits which proved their undoing…”

A credit reporting agency receives information from finance companies, banks and utilities, and adds it to your credit file. Those things worth reporting include arrears on a bill (usually more than 60 days late), missed loan repayments, new applications for credit, guarantees, litigation, change of job and address and defaults. Most of this information remains on file for around five years.

While an agency collects your credit history and gives you a score, it’s the lender you are dealing with who makes the final decision as to what kind of risk you represent.

There are a few steps people can take:

- Clean up: start by getting your repayments organised for credit cards, bills and loans. You can’t change history but you can influence your financial future.

- Job and house: take the easy points on a credit score and don’t change address or job for a year before applying for a mortgage.

- Applications: try not to apply for unnecessary credit. Typically people that chase zero balance transfer rates and change their credit cards multiple times each year can get scored down, so be careful.

- Get a report: you can go to the web site of a reporting agency such as Veda to access your credit report. Once you know your score – and the reasons for it – you can start planning.

- Broker: some mortgage brokers provide a free credit report because it will help determine which lenders will consider your loan application. If you’re working with a mortgage broker, be sure to ask about this service.

- Build the positive: changes introduced this year mean you get to build a score on positive credit behaviour. This means that every on time repayment is a small positive mark on your credit file. It’s worth thinking about how to take advantage of this.

Credit reports are a fact of life if you want to borrow money – they can be really helpful, so learn how they work and start planning. Good luck.

The post The importance of your credit score appeared first on .

]]>