The post A fundamental financial fact – time is money appeared first on .

]]>If there is one concept of finance and investing which is at the same time the most important and the least understood, it would have to be the time value of money. It’s the fundamental building block that the entire field of finance is built upon. And yet, many people lack a solid understanding of how it works.

Time value of money is the economic principal that a dollar received today has greater value than a dollar received in the future. If you were given the choice between receiving $100 today or $100 in 10 years, which option would you take? Clearly the first option is more valuable because of:

Risk – There is no risk of getting money back that you have today.

Purchasing Power – Because of inflation, $100 can buy more Mars bars today than it will in 10 years; and

Opportunity Cost – a dollar received today can be invested now and earn interest. However, a dollar received in the future cannot begin earning interest until it is received. This lost opportunity to earn interest is the opportunity cost.

All time value of money problems are solved using two fundamental calculations: compounding and discounting.

Compounding is the process of determining the future value of an investment made today and/or a series of regular payments.

Most people understand the concept of compound growth. If you invest $100 today and earn 10% interest for two years, your initial investment will grow to $121 at the end of year 2. The initial $100 compounds because it earns interest on the principal invested, plus it also earns interest on the interest.

Discounting is the process of working out the value in today’s dollars of money to be received in the future, as a lump sum and/or as regular payments, by applying a discount rate. The discount rate is the required rate of return or opportunity cost of an alternative investment.

It is impossible to make a sound investment decision without using these calculations, yet few do so accurately.

To illustrate with a simplified example, if a property you want to buy is worth $500,000 today and you require a 10% return, assuming you hold it for 10 years and receive a yield of 2% after all expenses, you would need to sell it for around $1.1m in 2025. To help work out if that is realistic, you could discount back from today’s value to 2005 at the same rate of return and compare it to sales prices at that time.

There are obviously a lot of other variables to consider, so, as always, see a professional before you invest. It could save you thousands.

If you would like to learn more about prudent investing, please send me an email or drop in for a chat.

If you would like to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post A fundamental financial fact – time is money appeared first on .

]]>The post Celebrating the wonders of the natural world appeared first on .

]]>Kelly Zarb:

“My work has a central theme of natural wonder and joy in colour. I feel a strong pull towards the moon, the stars and the sky. Every night after work I walk down my driveway, I look to the sky to see which of my friends are shining my way tonight. I feel that I am part of this vast universe. In order to capture this vast magical land and ocean of energy, I have developed a formula of geometric shapes including circles, triangles and repetitive dot sequences to explore unity, I can’t get enough of this grand science. These different elements create the backdrop for the universe at large which is the central theme of my paintings.”

Kelly Zarb: Embraced Beginnings, 30cm X 30cm, acrylic on canvas.

Bernadette Curtin:

“The sea creatures inhabiting the ocean, from tiny molluscs to the mighty whales, live in a majestic eco-system, each creature a part of the whole.

The coral reef systems, my focus for this body of work, symbolise the interconnectedness of all life, as well as the delicateness, preciousness and fragility of nature. If the way we live impacts on these systems and their inhabitants, how responsibly are we living?

The Ocean seems like a metaphor for a world uncorrupted, something we humans long for.”

Bernadette Curtin: Building the Reef, oil on canvas, 120cm x 90cm.

Merrilee Pettinato

“We have spectacular beaches in the Norther Rivers, each time I walk on the sand or swim in the sea the magic is all around me. Any one aspect of the ocean is worthy of expressing on canvas, and for this exhibition I have chosen to focus on the shoreline…a seagull strutting along the water’s edge, the crashing aquamarine wave with all the white crests, looking into a rock pool at the treasures living there, the pandanus growing in salty sand, the lighthouse a beacon of light to guide fishermen and sailors. The detail of random patterns, reflections and light play on the surface of the water, the colours that appear I find are of continuing fascination. When I break down a reflection the patterns, colours, light, shade and depth are so random…until you step back and view them as a whole and they then merge as water again.”

Merrilee Pettinato: Pier at Yamba, 120cm x 140cm, oil on linen.

![Land, Sea & Sky [1]](https://www.verandahmagazine.com.au/wp-content/uploads/2015/12/Land-Sea-Sky-1.jpg)

The post Celebrating the wonders of the natural world appeared first on .

]]>The post Campbell Korff on why it pays to have your glass half full.. appeared first on .

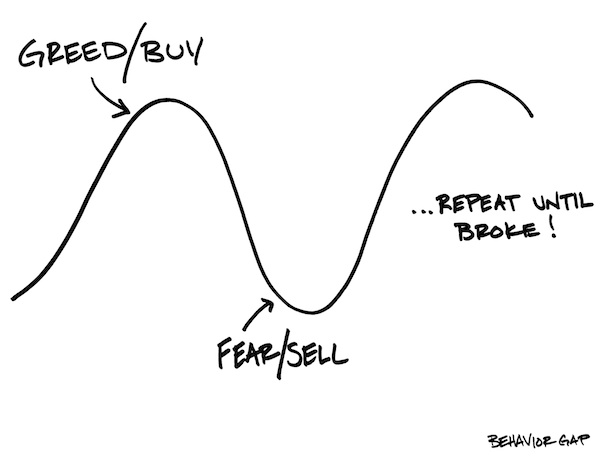

]]>It’s a well known face that we fear loss two to three times more than we enjoy gains. This psychology explains a lot of our behaviour in everyday life. Indeed, it has been critical to our survival for thousands of years.

Risk aversion can be very important when hunting for food in foreign environments, constructing a dwelling and caring for our young. However, when it comes to investing in the modern world it can lead to chronic underperformance. Here are a few reasons why:

Procrastination – fear of loss causes us to put off financial decisions in the hope tomorrow will be a better day. The problem for pessimists is that day may never come or be so delayed that more damage is done by leaving their capital on the sidelines.

Financial media – if we all felt great about the economy and our financial security we would never pick up a financial newspaper or watch the finance news each night. Our inherent financial insecurity has created a multi-billion dollar industry expert at exaggerating the most obscure financial data so long as it feeds our inherent belief that the financial world might just end tomorrow and send us all bankrupt.

Ignoring the facts – it is a fact that the Australian stock market has delivered average returns in the high single digits for over a century. It is also a fact that over this period only around 1 in 5 years produced negative returns. If you invested $10,000 in the Australian Stock Market in 1980 and re-invested the dividends, these facts would deliver you an investment worth around $850,000 today. You don’t believe me, do you? Our fear of loss causes us to discount positive data even when we know it’s true.

Short term thinking – we invest our savings across our entire adult lives. For most of us, this is a 60 to 70 year timeframe. Yet how often do we make decisions based on short term data? The Australian stock market is down around 15% since April, which is not good news if you need to sell your entire share portfolio tomorrow. If you don’t, history indicates it is more probably a time to think about investing more.

Compounding losses – there’s only one thing worse than losing money; that’s throwing good money after bad! Even when we know we have made a bad financial decision, we often stick our head in the sand in the hope the losses will miraculously disappear, rather than exit and stop the bleeding. Everyone makes mistakes. Face them, learn from them and move on.

Our fear of loss is instinctive, which makes it very hard to displace. However, to be successful investors we must be aware of how it can cloud our judgment and filter out information which is designed to accentuate this fear, rather than help us make good investment decisions.

If you would like to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post Campbell Korff on why it pays to have your glass half full.. appeared first on .

]]>The post The silver lining in the major bank rate rise appeared first on .

]]>The ‘Big Four’ banks all took the unusual step a couple of weeks ago of raising their mortgage rates by between 0.15 and 0.20% independently of the central bank. While by no means welcome news for homeowners, already nervous about a fragile economy, the rise will have a modest impact given the low base they rose from.

What the rise is really about, is the banks’ need to raise capital to sure up their balance sheets following APRA’s change to its capital adequacy requirements for banks in July this year. Obviously, if you are in the business of selling new shares, it is best to do it at a time when the prospects for future growth in earnings are good. If this is not the case, all you are doing is diluting existing earnings (from which dividends are paid) among more shareholders. The result: a lower share price.

For many reasons the opposite is currently true for the Big Four banks. So demonstrating to the market that they retain pricing power and are able to maintain their earnings, even in an unfavourable environment, will help the sales pitch for their new shares. For the time being at least.

The real winner out of this move is the RBA and, ultimately, the broader economy. Hitherto, the RBA was between a rock and a hard place: it needed to maintain low, possibly lower, interest rates to support a rebalancing of the economy but at the same time take the steam out of an over-heated metropolitan property market. Ongoing constraints in the supply of new homes and limited influence on lending policies, made this task almost impossible.

Fortunately, in an unintended act of altruism, the Big Four have raised rates and signalled that they might do so again. They have also had to, belatedly, tighten their lending to property investors. This has sent buyers in Sydney and Melbourne back to their spreadsheets.

Thus, the way is now clear for the RBA to maintain, if not further reduce, the cash rate to support the services sector and exporters (who will benefit from a resultant lower dollar). All good news for the Northern Rivers economy.

If you want to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post The silver lining in the major bank rate rise appeared first on .

]]>The post Win $5000 and a mentoring session with Mark Bouris appeared first on .

]]>

Verandah Promotion

Do you want to meet renowned Australian businessman, media personality, chairman of Yellow Brick Road, and this seasons host of Celebrity Apprentice, Mark Bouris?

Yellow Brick Road Ballina are offering you the chance to meet with Mark Bouris for a one hour mentoring session where you can get Mark’s personal insights into being successful. They are also throwing in a hefty $5,000*

For your chance to win, register with Mark’s trusted advisers at Yellow Brick Road Ballina for an obligation-free 15 minute financial health check.

In your financial health check, your advisor will look at what your financial goals are, where you are now and help to start you on your journey to a secure financial future.

Contact our Ballina branch on 02 6686 6678 for your obligation-free health check and we can get you started on your path to financial freedom.

* Competition Terms and Conditions apply. Credit services provided by Yellow Brick Road Finance Pty Limited ACN 128 708 109, Australian Credit Licence 393195. Financial Planning services provided by Yellow Brick Road Wealth Management Pty Limited ACN 128 650 037, AFSL 323825.

The post Win $5000 and a mentoring session with Mark Bouris appeared first on .

]]>The post Raw fish, and hold the chips… appeared first on .

]]>John Wickens used a Nikon D7200 camera with a Nikkor 18-300mm lens. His photos are available for viewing on his facebook page, and he can be contactated by email on [email protected]

The post Raw fish, and hold the chips… appeared first on .

]]>The post Asking yourself the uncomfortable ‘what if’ questions appeared first on .

]]>

To protect your family, Campbell Korff from Yellow Brick Road suggests that you ask yourself the uncomfortable ‘what if’ questions.

The life insurance industry has been in the spotlight recently. The commission structures paid to brokers and advisers by insurers have been accused of causing excessive ‘churning’ (moving clients to a new insurer unnecessarily), because a large portion of the commission was paid on issuance of the policy. While the restructuring of these commissions to a longer term and flatter structure was right, in my view, it missed an opportunity to address the much bigger issue of why Australians remain chronically under-insured.

The regulators and insurers only have themselves to blame in this regard. For too long life insurance was ‘sold’ to people using aggressive marketing techniques by networks of agents and thinly qualified advisers rewarded by very large commissions. The innate Aussie suspicion of the salesman and the big institution operated to thwart these efforts and has placed the insurance industry near used cars and real estate as the professions least loved.

The problem is that there is now a huge number of people that live with the risk of being wiped out financially every day but are either totally oblivious to it or choose to ignore it. Others believe they are covered but have inadequate or inappropriate cover.

Personal risk management is a key component of everyone’s financial affairs. It is a complicated area and you should seek expert advice from an independent professional, however, the following summarises some of the key principals:

- Your future income is your biggest asset, so before you insure your boat, car or even your house, insure yourself. Even for people on modest incomes, you may need to invest an insurance lump sum of over $1million to replace your future income.

- Many people think ‘it’ will never happen to them. Google the statistics. Odds are ‘it’ will before you retire. More importantly, think about the downside for your family if ‘it’ does and you are not covered.

- Ask yourself the ‘What if’ questions:

‘What if something happens to my partner’s health and he/she:

- a) dies

- b) can’t work for 6 months

- c) can’t work ever again

- d) needs emergency surgery, how would the family cope financially?’

Make sure your partner does the same.

- There are four types of personal risk insurance: life, total permanent disability, income protection and trauma cover. Each is designed to help you address these ‘What if’ questions. Getting the balance right requires a technical understanding of each and your personal circumstances and risk tolerance. This is your adviser’s job.

- Like most things, with insurance you get what you pay for. If it’s cheap, there’s a reason: it doesn’t cover as much.

- The ‘default’ insurance cover provided with most industry superannuation funds is rarely adequate for a family with children and debt.

- If you have existing insurance, think carefully before switching to a new insurer. If you have suffered health problems or changed your lifestyle, the new insurer may not provide the same breadth of cover as your existing one.

- Always pay your premiums on time and never cancel a policy before a replacement has issued.

If you want to contact Campbell Korff of Yellow Brick Road Ballina go to: www.ybr.com.au/Branches/Ballina

The post Asking yourself the uncomfortable ‘what if’ questions appeared first on .

]]>The post What are you waiting for? appeared first on .

]]>

With home loan interest rates at record – and expected to stay that way for a few years to come, Mark Bouris of Yellow Brick Road Management is surprised not more Australians are taking advantage of the situation.

I’m more than a little surprised by the results of a survey we recently completed. We reviewed the situation of one thousand Australians who’d obtained a home loan more than two years ago.

This is what we learned: 40 percent of those surveyed said they had never refinanced. Another 19 per cent hadn’t refinanced in over five years, six percent had refinanced four to five years ago, eight percent had three to four years ago and 10 per cent had between two to three years ago.

This is the situation: interest rates are at their lowest in over 50 years, yet 83 percent of Australians with a home loan have not refinanced in the past two years!

I find it hard to believe that so many people are avoiding action. The newspapers are full of stories about the historically low interest rates and the potential savings available to people with home loans.

It’s outrageous that people are still paying high interest when the opportunity to pay less is right under their noses. People take the time to drive to the cheaper grocery store just so they don’t pay an extra dollar for milk, yet when it comes to home loans they stick their head in the sand.

‘In effect, a failure to refinance to the best interest rate means

you’re just handing the banks extra money.’

Reserve Bank of Australia data shows the benchmark 2.0 per cent interest rate is significantly lower than the average of 5.13 per cent that Australians experienced between 1990 and 2015. The all-time peak was at 17.50 per cent in January of 1990.

Because of certain business practices, most bank mortgage rates have not reduced in line with official interest rate reductions. A typical 2010 loan may today be on a current variable rate of around 5.3 per cent, whereas rates are now available at around 4.8 per cent, or better.

Even allowing for fees and transfer costs, it is likely that those on a home loan secured a number of years ago could make monthly savings by switching lender.

For those who took out a home loan five years ago, the average rate after reductions would be 5.3 per cent. The potential savings on an average $350,000 loan with 25 years remaining could be thousands. For example, if you refinanced to a rate of 4.8 per cent, you would save $30,660 in interest over the remaining life of your loan.

There are lenders offering rates as low as 4.1 to 4.2 per cent, so your savings could be greater.

According to our survey, people avoided refinancing because they didn’t believe they’d save enough money, they thought the fees and charges would outweigh the benefits and they perceived the process to be too much of a hassle.

I just don’t buy this. With interest rates dropping to a low that no one in my generation would have thought possible, it’s crazy to not find out if you can save. If you don’t have the time or the expertise, speak to a mortgage broker and let them investigate a refinancing deal for you.

It’s also worth remembering that when interest rates do finally start edging up, those who already have the best home loan deals will have a natural buffer against interest rate rises.

At least our survey found that the younger generation are on the ball: 28 per cent of 25-34 year olds refinanced in the past two years compared with 13 per cent of 45-54 year olds.

Is this because young people are more internet-savvy and accustomed to comparison-shopping for the best price? Perhaps, and good on them.

If you’re in the majority and haven’t refinanced for years, let me leave you with this: a home loan is the largest monthly outgoing for most households, and if you’re paying too much – when interest rates are historically so low – you’re burying your head in the sand.

Mark Bouris is the Chairman of Yellow Brick Road Management. If you want to contac tCampbell Korff of Yellow Brick Road Ballina go to: ybr.com.au/Branches/Ballina

The post What are you waiting for? appeared first on .

]]>The post Under the Boardwalk… appeared first on .

]]>

“I took this from the Point pub below the Ramada in Ballina on a Friday night,” says Ballina resident Greg Lloyd-Smith. “I regularly meet for a couple of drinks with some friends there, and the sunsets on the river are spectacular. The boardwalk is also a great Ballina institution – it winds its way from below the RSL Club to the Yacht club, and it’s well used by people exercising or fishing, or out with their kids, or simply sitting and looking at the river.”

The photograph was taken on a Nokia Windows phone with a Zeiss lens.

The post Under the Boardwalk… appeared first on .

]]>The post Transitioning towards a rosier retirement appeared first on .

]]>

If you are in or nearing your 50s and unsure of whether you have enough savings to retire on or simply want to accelerate your retirement savings, making use of a Transition to Retirement Pension (TTRP) can be a very effective strategy writes Campbell Korff from Yellow Brick Road Management.

Since 2005, the superannuation rules have allowed people nearing retirement to supplement their income by drawing up to 10% (and a minimum of 4%) as a TTRP. The rationale is to encourage people to work longer by allowing them to reduce their hours and top-up their income from superannuation.

However, for those willing to continue to work full-time through their 50s and 60s, these rules present an opportunity to take advantage of the highly favourable tax concessions applicable to superannuation contributions, earnings and income.

The basic strategy is to salary sacrifice as much as you can into superannuation (up to $35,000 if you are over 50) and draw back out of superannuation only what you need to live on as a TTRP. This strategy can also be used by self- employed persons in a similar manner.

The main benefits of implementing a TTR strategy are:

- Pre-tax income contributed to superannuation (within the Concessional Contributions Cap) is taxed at 15%, instead of your marginal income tax rate if you do not save into superannuation. In many cases, more than halving the income tax rate on the amount contributed;

- Earnings tax paid inside of superannuation can be eliminated by using a TTRP. This effectively adds 15% to the performance of your retirement savings each year;

- Tax friendly income derived from the TTRP will allow you to salary sacrifice more into superannuation than you need to take out. Income derived from a TTRP is generally more tax effective than income received from working, especially after age 60. This can open up an ‘arbitrage situation’ where the amount needed to draw from the pension is much less than the amount needed to replace it via salary sacrifice;

- The TTR strategy can result in lower taxable and assessable income. This can enhance the ability to qualify for tax offsets such as Mature Age Tax Offset (MATO) and Low Income Tax Offset (LITO);

- The strategy can be completely unwound (i.e. funds rolled back to superannuation);

- The level of income received can be adjusted between minimum and maximum levels; and

- This is a tax driven strategy. This means it is not reliant on strong market performances to make it a successful strategy.

If you would like more information on preparing for or implementing a TTR strategy, contact your wealth manager.

If you would like more information on these issues, drop me an email at [email protected]. Or visit the YBR Ballina website on: ybr.com.au/Branches/Ballina

The post Transitioning towards a rosier retirement appeared first on .

]]>